|

Dear Scarsdale Community,

I am writing to you today to share important information about the work underway to develop our 2026-27 school budget. On Monday evening, the Board of Education is scheduled to meet for the third and final Budget Study Session related to the proposed 2026-27 school budget. During that meeting, the District Administration anticipates presenting a tax cap compliant budget. Arriving at this budget has required difficult choices, and I want to communicate as clearly as possible the rationale for decisions that we will present and discuss during the meeting. I know that the budget process is not something everyone in our community tunes into regularly, so I hope you find this helpful. The message is followed by several frequently asked questions in case you are interested in a deeper understanding of the situation we find ourselves in.

Members of our community who have followed school budgeting for a long time will recognize that the process has been more strenuous and difficult over the past several years. Historically, Scarsdale has been a district that has been appropriately resourced which has enabled program innovation, expansion to take place while maintaining outstanding educational outcomes. This community has shown a level of financial support that reflects the real cost and value of an exemplary public education, more so than in many (dare I say most?) other places. In recent years, however, our ability to do more has been restricted by the normalization of 2% growth brought about by the tax cap. In fact, in some ways we are doing the same with less, as the pace of inflation has outstripped the growth of our budgetary resources (click here for a good NYSSBA article about this). While a tax cap override is a tool available to the Board, I believe evidence suggests it is a tool to be used judiciously and prudently. An unsuccessful budget vote is a worst-case scenario. Our community did support a significant override (4.45% tax increase) in 2024. This year, we are asking the community to not only support a budget, but also a $101 million bond referendum to make much needed capital improvements to aging buildings across our district. With that as background, I invite you to read on to learn more about where we stand with respect to the 2026-27 proposed budget.

Sincerely,

Dr. Drew Patrick

Superintendent

About the Process

The annual budget deliberation process unfolds over many months, and starts with an analysis of where we currently stand (thus the budget freeze initiated this week). We seek input on needs and wants in late fall and early winter, and develop an initial proposal for staffing and all other budget components. The public part of the process involves four major presentations and discussions. Below are links to these public presentations as a point of reference.

After each presentation, there is discussion, public comment, and a direction given to the Administration. While the Administration is responsible for preparing and proposing the school budget, it is ultimately the Board of Education that determines the budget that will go before voters. Toward the end of the process, the Board holds a Public Budget Forum (March 23, 2026), and ultimately adopts the budget. This year, budget adoption is scheduled for the April 13, 2026, Board of Education meeting. Once the Board adopts the final budget for the 2026-27 school year, it will be up to voters to weigh in on May 19, 2026, at SMS from 7 AM to 9 PM.

Expenditures and Revenues

As with any budget, we can’t spend more than we take in. Thus, the maximum we can spend is directly tied to how much revenue we collect. 92% of our revenue comes from tax levy, which is the highest in the region. Our other revenue sources, including State aid, county sales tax, tuition, and interest income, account for only 8% of our revenue. Thus, our ability to fund the expense budget is almost entirely dependent on taxing our community, and our ability to do that is strongly influenced by the legal tax levy limit, better known as the tax cap.

2026-27 Tax Cap Calculation - Allowable Tax Levy Increase = $5.9 million

This is the so-called “allowable” tax increase over the current fiscal year that remains compliant with the State’s tax levy limit. More familiarly known as the tax cap, it is the amount of funding we can ask from our taxpayers that only requires a simple majority (50% +1) of “yes” votes to approve the budget. An increase larger than this amount requires a 60% supermajority of “yes” votes. For next year, all other sources of revenue are projected to increase by a total of only $16,000. Thus, essentially all spending above the current year amount needs to come from tax levy, which can only supply an additional $5.9 million over this year without a supermajority.

“Status Quo” Cost Increases

Before doing anything new or different, the following costs are increasing as a result of forces mostly outside of our control, as they are mandates or contractual obligations.

Category |

Cost Increase |

What This Includes |

Health Insurance |

+2.8 million |

health claims, stop loss insurance, admin fees |

Social Security & Medicare (FICA) |

+400,000 |

federal payroll taxes on employers |

Salaries and Wages |

+3.0 million |

negotiated contract increases |

Contractual |

+1.1 million |

student services, liability insurance, vehicle maintenance |

These are the areas with largest year over year increases. There are dozens of modest increases (often <2%), and even decreases, in many other areas of the budget. Nonetheless, without doing anything new or different, we will exceed our tax levy limit by $1.4 million just in these categories alone. As a result, bringing a budget at or below the limit requires that we reduce expenditures from what we presented at the start of the budget process (see February 9, 2026). In some cases, those reductions will result in flat year-over-year budgets in specific areas. In other cases, the reductions will mean less spending or fewer staff members next year than this year. During Monday’s meeting, we will be discussing the reductions we have proposed to reach the spending limit. These changes are summarized below.

Anticipated Spending Reductions Since March 2 Budget Study Session #2

The list below includes the $1.9 million in reductions necessary to lower the proposed expenditure budget to the tax levy limit.

Category |

Reduction Amount |

Description of Reduction |

Benefits |

$671,308 |

Revise health budget down as a result of better performance in our prescription drug plan and anticipated reduced stop loss insurance; benefit reductions based on elimination of positions (see below) |

BOCES |

$32,500 |

Elimination of Zoom licenses (use Google Meet instead), reduction in Smart Notebook accounts; reduction in Schoology support |

Contractual |

$187,696 |

Defer original proposal to add 1.5 social workers to the elementary level; miscellaneous technology reductions (software support/training) |

Staffing |

$929,169 |

Defer additions of 1.0 Math (SHS) and 1.0 SPED (SMS); reduce 1.0 secretarial (vacant - SHS); reduce 1.0 tech services; reduce Teacher Aide staffing (attrition); reduce 2.0 elementary sections (enrollment); Summer program improvement ( remove proposed increase of $40k and decreased budget by additional $80k) [Note: 1.0 ENL position (attrition) was cut in initial February 2 proposal] |

Supplies |

$88,750 |

Reduce food allowance for Sup't Conf Days (lunch on your own); reduce SPED testing materials replacement quantity remove proposed furniture purchases; defer increase in funds for student activities (SHS) |

Technology |

$76,034 |

Reduce technology hardware procurement |

Budget Summary

Below is the anticipated year-over-year comparison and budget summary for the 2026-27 school budget.

Category |

2025-26

Approved Budget

|

2026-27

Revised Draft Budget

|

Budget to

Budget Difference

|

% Change |

Total Expenditures |

$191,504,833 |

$197,098,146 |

$5,593,313 |

2.92% |

Other Revenues |

$13,219,478 |

$13,235,472 |

$15,994 |

0.12% |

% of Total Budget |

6.90% |

6.72% |

|

|

Transfer from Reserves |

$1,281,233 |

$1,031,233 |

-$250,000 |

-19.51% |

Assigned Fund Balance |

$1,190,900 |

$1,100,000 |

-$90,900 |

-7.63% |

Total Tax Levy |

$175,813,222 |

$181,731,441 |

$5,918,219 |

3.37% |

% of Total Budget |

91.81% |

92.20% |

|

|

Some Frequently Asked Questions

Why are we in this difficult budget position? What has changed?

Since its passage in 2011 and subsequent implementation, the “Real Property Tax Levy Limit” bill has created an arbitrary ceiling on property tax levy increases to the lesser of 2% or the rate of inflation. While Boards of Education can present a budget to voters that exceeds the limit (cap), this requires a 60% supermajority for approval. Scarsdale has put up budgets in excess of the cap twice since being signed into law - once defeated (2013) and once supported (2024). Staying within the cap the majority of the time has led to downward pressure on the budget, and has forced difficult choices as expenditures have been growing faster than the tax levy cap allows. This scenario leaves us with only a few choices: reduce expenditures (i.e., make cuts), use fund balance (the “rainy day” fund), and/or ask the voters to override the tax cap. More explanation about each of these choices appears below.

It seems like we have had to make more cuts in recent years. Why?

From 2015-16 to 2020-21, the approved budgets were below the tax levy cap by an average of $733,000, totaling $4.4 million over that time. While these budgets were carefully developed and scrutinized, they also resulted in reduced budget flexibility year-over-year. Then, as you know, Covid ushered in a period of extremely high inflation. With the allowable tax levy limit capped at 2%, our already-reduced flexibility became something of a crisis. Eventually, the Board decided that they needed to adopt a budget over the cap, and did so by $1.34 million in the 2024-25 school year, which the community supported. However, even that budget resulted in cost reductions to offset the inflationary growth experienced in many areas of our operation.

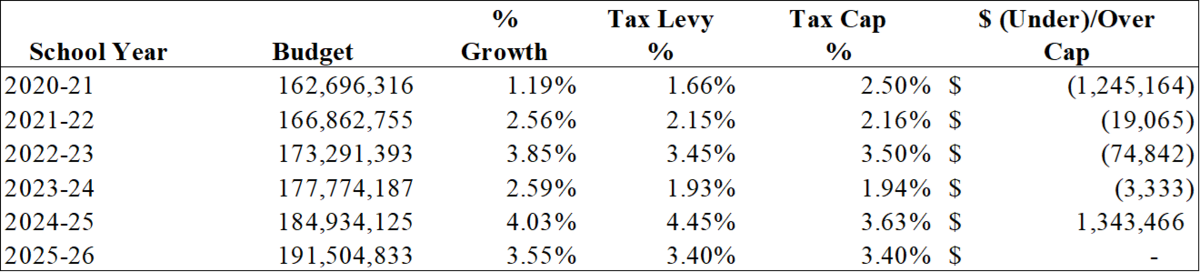

The current 2025-26 school budget was adopted at the tax cap, but expenditure reductions were again necessary, and primarily came from the net reduction of 6 faculty and staff positions. Below is a summary of the past six years, which illustrates the shift to budgets at or above the cap versus well below the cap (2020-21).

It is important to note that in any given year, the allowable tax levy growth is dependent upon the prior year levy (i.e. lower levy = lower growth; higher levy = higher growth). Thus, leaving money “on the table” limits revenues in the subsequent years.

How do we determine what to cut? If we have to cut, can’t we avoid cutting staff?

Fully 80% of our budget goes to salary, wages, and benefits. Beyond that, we have mandated services, mandated transportation (including to private schools up to 15 miles away, and special education programs up to 50 miles away), utility costs, etc. The portion of the budget outside of staffing that is discretionary is very small. This cost distribution essentially makes it impossible to reduce expenditures without reducing the number of positions in the district, or paying for new positions or programs by phasing out existing positions or programs. However, we have made every effort to eliminate positions through attrition, rather than layoffs, whenever possible. While we have made reductions in all areas of the budget over the past several years, our ability to reduce these other areas has a limit.

Why don’t we just use fund balance (our rainy day fund) to get through this period?

First, a quick primer on fund balance. By law, we are allowed to maintain two types of fund balance - money in designated reserves for designated purposes, and a more general “unassigned” fund that can total no more than 4% of the subsequent year’s budget. The designated reserves are best used to smooth out what would otherwise be spikes and dips in budgets year-over-year. Two easy to understand examples are the retirement reserve and the health plan reserve. When mandatory contribution rates to ERS or TRS (employee retirement system, teacher retirement system) spike, the reserve is used to limit the impact on the overall budget. When the rates go down, funds are put back into the reserve for a later date. We treat the health reserve in the same manner, though the nation-wide escalation in health costs has made that challenging.

The undesignated fund is really our emergency fund, and we strive to maintain that 4%, in part because our credit rating and ability to borrow is tied closely to the health of this fund. Nonetheless, we regularly appropriate fund balance to help pay for the budget. Historically, the District has generated surplus (revenues > expenditures), and has used that surplus to help fund the next year’s expenditures - to the tune of $1.1 million annually - while staying at or close to the 4% level. If we were to stop doing that, we would immediately have a $1.1 million gap to fill (i.e., it would require more cuts or the need to find different revenue). If we were to increase that amount, we would have to maintain that increased amount over time, or have a gap to fill by that amount in the next year’s budget (i.e., cuts or different revenue). The steady year-to-year assignment of this amount allows for predictability. The designated health reserve, on the other hand, has been going in one direction in recent years as healthcare costs here and across the country have risen by as much as 10% annually. With a health claims budget in excess of $25 million, a 10% increase equates to $2 million in additional costs. It is growing far faster than the tax cap can support. However, if we were to deplete the reserve, we would be even more reliant on the tax levy to meet our health obligations to employees. Thus, we are seeking to slow down our reliance on the health reserve, and to put surplus back into that reserve when possible.

Why don’t we just exceed the cap and ask the community for an override?

Since the so-called “tax cap” was implemented, budget approval rates state-wide have steadily increased. However, a closer examination of the data suggests that the vast majority of defeated budgets are those that exceed the cap. For example, in the most recent budget vote in May 2025, voters across the state approved 96.5% of school budgets - 654 passed and 24 were defeated. However, of the twenty-four districts that experienced a budget defeat, seventeen were attempting to pierce their Tax Levy Limit and therefore needed a super-majority (60 percent) for approval. Twenty-five districts were successful in their Tax Levy Limit override attempt, just as we were in 2024. Voter data suggests that budget growth in an amount at or around the 2% level has become normalized around the state, as voters are “trained” to think of the cap as normal. We care deeply about the impact of school taxes on our community, and strive to strike a balance that maintains our exceptionally high-quality of education and allows for innovation and improvement while minimizing the impact on our tax paying community.

How does the proposed $101 million Bond impact the budget?

First and foremost, the proposed 2026 Capital Projects Bond has no impact on the 2026-27 budget. The costs of the bond wouldn’t come into play until the 2027-28 budget. If authorized by the public on May 19th, the 2026 Capital Projects Bond will impact the budget over a period of years by raising the amount the District owes in principal and interest payments on borrowed funds, not unlike a home mortgage loan. However, principal and interest payments on borrowed funds are excluded from the tax cap calculation. In other words, while the cost of borrowing does increase the budget, that incremental cost is excluded from the determination of how much the tax levy can grow from year to year. Thus, the borrowing does not functionally impact our funding for the instructional program. Said another way, avoiding these borrowing costs does not free up any funds for the portion of the school district budget that funds teaching and learning. Furthermore, avoiding these borrowing costs now would defer the need for ever greater investment in the future as our buildings and facilities reach the end of their useful life.

|